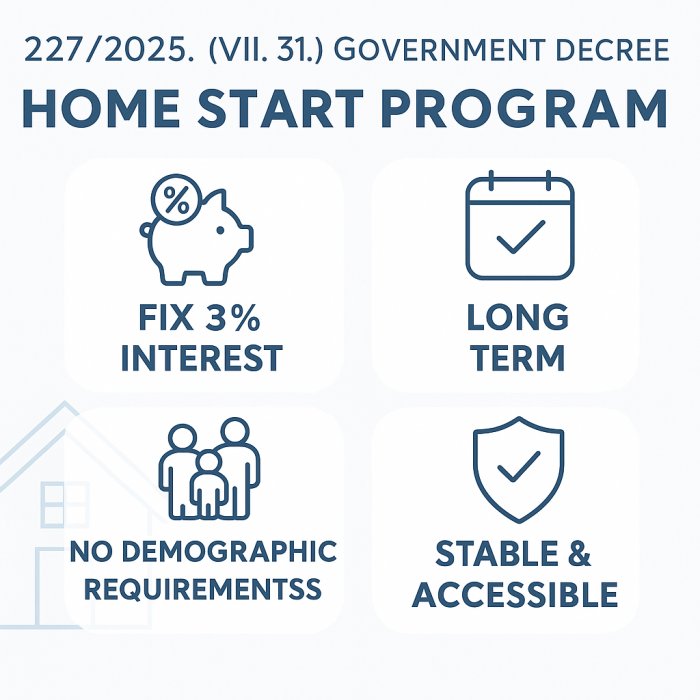

On July 31, the Government Decree 227/2025 (VII. 31.) entered into force, introducing a new form of state support: the FIX 3% interest housing loan available under the Home Start Program. The purpose of the regulation is to help young people acquire their first home and to provide a financing option that ensures security and predictability in the long term.

Below we present in detail the key features of the program, the eligibility criteria, the possible uses and the practical information.

Main parameters of the loan:

- Interest rate: fixed 3% (unchanged throughout the term)

- Maximum loan amount: HUF 50 million

- Maximum term: 25 years

- Currency: HUF

- Purpose: primarily for the purchase of a first home or the construction of a new one

The fixed interest rate is a particularly important factor in the current economic environment. In the case of market-based loans, variable interest rates are common, which can pose significant uncertainty for families in the long run. By contrast, the 3% fixed rate ensures predictable, stable repayments.

Who is eligible for the loan?

According to the regulation, the loan is primarily available to first-time homebuyers or builders. One of the biggest advantages of the scheme is that it is not tied to demographic conditions:

- no marriage required,

- no mandatory childbearing,

- no specific family status requirements.

This is a significant difference compared to earlier forms of support (e.g. CSOK, Babaváró), which mainly aimed to encourage childbearing. The new program focuses instead on the security of housing, extending the opportunity to those who are still in a pre-family stage of life.

It is important to note, however, that an applicant can only benefit from this subsidized loan once in their lifetime.

What type of property is eligible?

The loan clearly aims to support homeownership. Accordingly, it can be used for:

- the purchase of a first home,

- the construction of a new home,

- in certain cases, the extension of a dwelling, provided it increases the living space.

In the case of new construction, it is a specific requirement that the bank must verify that the overall budget is fully secured and that the subsidy is not intended to cover an already underfunded project. This means the applicant must provide detailed documentation of the implementation costs and sources.

How does the support work?

The essence of the scheme is that the state provides interest rate support compared to the market level, resulting in a fixed 3% rate for the borrower throughout the term of the loan.

This has two major advantages:

- Stability – the repayment instalment remains unchanged throughout the loan term, allowing borrowers to plan with certainty.

- Affordability – the conditions are generally much more favourable than market-based loans, especially for long terms.

What should applicants pay attention to?

Although the regulation provides favourable conditions, there are several practical considerations to keep in mind during the application process:

- Creditworthiness: the bank will still assess the applicant’s income situation, and the JTM (income-to-debt service ratio) rules apply.

- Property valuation: the market value of the property serving as collateral is determined by an appraiser.

- One-time opportunity: the applicant can only use this option once, so the decision should be carefully considered.

- Documentation: in the case of new construction, the full budget and financing background must be presented in detail.

- Preliminary legal review: checking the legal consistency of the loan agreement and the real estate sales contract is essential to avoid later disputes.

Why is this program an advantage?

The FIX 3% housing loan program could mark a new era in Hungarian homeownership support for several reasons:

- Broader access – without childbearing or family status conditions.

- Long-term predictability – repayments remain unchanged for up to 25 years.

- Support for young people’s independence – allows young adults to acquire their own home before starting a family.

- Transparency – the regulation clearly defines the conditions, enabling applicants to plan ahead.

Summary

Even with the favourable conditions of the Government Decree 227/2025 (VII. 31.) introducing the Home Start Program, it remains essential that every detail of the real estate sale and purchase agreement related to the loan is legally sound. Based on our law firm’s experience, even a minor mistake or omission may carry significant risks later on. Therefore, we recommend entrusting us with the drafting and review of the contract, so you can be confident that your transaction will be secure and legally compliant in every respect.

If you require assistance with drafting the contract, please do not hesitate to contact us for an appointment at one of the following:

E-mail: info@radvanszki.eu

Phone: +36 30 475 3115